I’ve just returned from the cinema where I went with my sister to see Toy Story 3. It may be about talking toys but it was filled with some wonderful script writing and it’s a thoroughly enjoyable film.

I’ve just returned from the cinema where I went with my sister to see Toy Story 3. It may be about talking toys but it was filled with some wonderful script writing and it’s a thoroughly enjoyable film.

Amidst the humour and tension there are some powerful life lessons so here’s a few I picked up and how they relate to growing your pennies!

This post contains spoilers so only read if know or want to know the plot

Mistakes happen

Buzz and other toys should have been safely put away into the attic when Andy heads off the college. Instead, his Mum takes the toys out to the curb. Like the other Toy Story films the plot is driven by an accidental mistake happening and the attempt to put things right.

Life, for both the toys and ourselves, rarely goes smoothly.

Mistakes do happen. Yet the toys never give up in their mission to get home. Their determination is admirable and is a lesson for us all.

You will make mistakes (with your money and otherwise), the hard, but most important part, is that you pick yourself up and get your focus back.

The power of a well-executed plan

Escaping from being taken away with the trash, the toys take refuge in a box destined for day-care, but after reaching their destination, find that the centre is not what it seems.

They are trapped in a room with only a small window high above them.

It’s impossible for a toy to reach.

But, moments later, Buzz is flying through the air -or rather, falling with style – catapulted by a series of aerial stunts, to the promised land of the open window. It is a true testament to the power of a well-executed plan.

Just like looking at an impossibly high window, we face our own challenges in life: thinking about all the different things we need to buy in the coming years can be daunting. Cars, houses, weddings, retirement…it may seem unachievable sometimes. But if, like the toys, you develop a game plan, then with a bit of luck and creativity, you’ll get there.

Spend on the things that matter to you, not anyone else

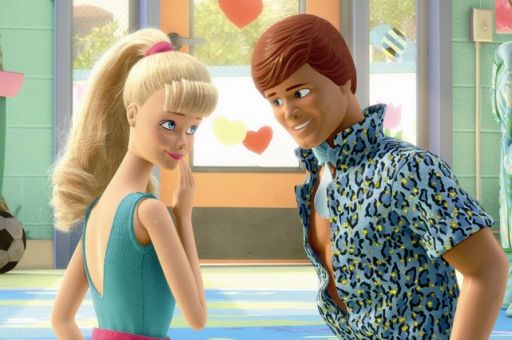

Ken is teased for his extensive clothing collection. From an outside perspective it seems ridiculous to have so many outfits to wear but Ken is delighted when Barbie gives him the opportunity to wear them.

Many of us have the equivalent of Ken’s wardrobe. We spend our money on things that our friends or family don’t understand: perhaps piles of books, shiny electronics, or flash cars?

People often think personal finance is about cutting back, being sensible with your money.

It’s not.

It’s more about being conscious with your spending. Certainly you should make sure you’re saving for your goals in the short and long term, but you should also not feel bad spending money in the present on the things that matter.

But also remember, Ken might have enjoyed his ‘stuff’ but he had even more fun when he had someone to share the experience with. As Suze Orman says: “People, then Money, Then Things.”

Mix it up a bit -you might just like it

Mix it up a bit -you might just like it

In the midst of the adventure and daring escape, Buzz is reset to factory settings and reboots into a Spanish version of himself, much to Jessie’s delight.

Buzz’s Spanish transformation offers a much needed comedic element easing the tension that has built up, and Jessie finds a whole new side to Buzz, changing the way she feels about it forever!

Similarly in life, random events and meet ups happen all the time and can send your life down a whole new path. Being in control of your money makes it much easier to follow these opportunities. Certainly a budget helps you stay focused but it also allows you to ‘mix it up’ a bit which time and again can lead to a more fulfilling and fun life- and who doesn’t want that?

-To use a personal example, in recent weeks my budget has allowed me to head off to Ireland for an evening, and I’m heading to NYC in September!

It’s never too late to redeem yourself

Towards the end of the film, Ken sees the error of his ways and switches allegiances to Woody and the gang. It’s a risky move but Toy Story 3 teaches us that it’s never too late to be redeemed from poor judgement in the past. Woody even gives the evil, strawberry smelling, teddy bear an opportunity for redemption.

Likewise it’s never too late to redeem yourself from poor money habits or judgements you have made in the past. The sooner you get started on the right path to growing your pennies, the more time you have for your savings to grow.

Life goes by so fast

I remember when Andy was young, playing with Woody and Buzz in the first Toy Story film. By Toy Story 3, Andy has grown up and is moving to college. Life goes by so fast!

- You may think you’ve got ages until retirement or before you get started on the property ladder but it will come around so so fast.

- You may think you’ll begin saving when you’re earning more money.

- You may think you’ll start learning about investing when you have a little more time.

But, like Andy, you’re growing up fast

Toys fear their owners growing up and not playing with them anymore. Thankfully we don’t have to fear the future. Follow through with a plan and we can embrace it.

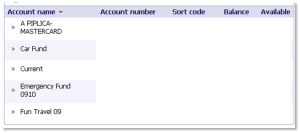

One of the most common ways to gain a perspective on your spending is by keeping a picture in your wallet. Every time you look in your wallet to spend, you are forced to look at the picture. Perhaps it’s a photograph of your family. Or a picture of your dream house cut out of a magazine. Whatever it is, it should be something that will make you question whether the money you are spending right now is worth being one step further away from your goal.

One of the most common ways to gain a perspective on your spending is by keeping a picture in your wallet. Every time you look in your wallet to spend, you are forced to look at the picture. Perhaps it’s a photograph of your family. Or a picture of your dream house cut out of a magazine. Whatever it is, it should be something that will make you question whether the money you are spending right now is worth being one step further away from your goal. Many banks (especially those with online operations) allow you to rename your accounts. By naming an account for a specific item it can help you compartmentalise your savings, making it harder for you to justify spending them away.

Many banks (especially those with online operations) allow you to rename your accounts. By naming an account for a specific item it can help you compartmentalise your savings, making it harder for you to justify spending them away.

A lot of personal finance is about cutting back, doing without -you know – saving.

A lot of personal finance is about cutting back, doing without -you know – saving. It started innocently enough. Yesterday morning regular reader and friend The Other Adam sent an group email to a few of us as he’s decided to get a new phone. A few suggestions came back and I casually googled the phones. And promptly fell in love.

It started innocently enough. Yesterday morning regular reader and friend The Other Adam sent an group email to a few of us as he’s decided to get a new phone. A few suggestions came back and I casually googled the phones. And promptly fell in love. In the past I’ve not used my phone much but in recent months my usage has increased -I’ve enjoyed catching up with old and new friends and also started using the internet on my phone a lot more.This has been become more costly than originally calculated so if my usage were to stay the same a contract phone would be more economical.

In the past I’ve not used my phone much but in recent months my usage has increased -I’ve enjoyed catching up with old and new friends and also started using the internet on my phone a lot more.This has been become more costly than originally calculated so if my usage were to stay the same a contract phone would be more economical.