The following is a guest post by Liz Goldman for Sunbird FX – the currency trading specialist and CFD broker.

According to a U.S. government survey, making better financial decisions is one of the top new year’s resolutions made by Americans, along with vows to lose weight and get more exercise. It’s a great time to make sure you’re getting 2012 off to a good start financially. Here are some ways to give yourself a financial check-up:

According to a U.S. government survey, making better financial decisions is one of the top new year’s resolutions made by Americans, along with vows to lose weight and get more exercise. It’s a great time to make sure you’re getting 2012 off to a good start financially. Here are some ways to give yourself a financial check-up:

Shop around for better interest rates

Interest rates on savings accounts are rock bottom right now, so it’s particularly important to do the best you can. Check local banks, credit unions, and online financial institutions. Make sure there are no fees or hidden terms. Some accounts that look good on the surface are bad deals when you read the fine print.

Shop around for better credit card terms

Banks tightened up on lending, dropping credit card limits and closing accounts, during the worst of the recession. Now many are looking for new customers and dangling attractive introductory rates and reward programs to entice them. The best credit cards often have annual fees, so make sure you’ll get enough benefits to make the cost worthwhile. Ask if the card issuer will waive the fee for the first year. If you find a card with a zero interest promotion, transfer a balance from a high interest card.

Pay more money on your highest interest credit card account

Interest eats up a big chunk of your monthly credit card payment if you’re only paying the minimum due on that card. You’ll lower the actual balance more quickly if you channel more money toward a high interest account. It’s gratifying to see the balance drop more quickly, and once you pay off one of your cards, you can use that extra money to tackle another high interest bill.

Increase your savings

It never hurts to have a money cushion for unexpected bills like car repairs, dental emergencies, or anything else that suddenly causes a major expense. A hefty savings account also cushions you against the effects of a crisis like job loss. Determine how much you can afford to pay each month. Write a check and deposit it into your savings account at the same time you pay your monthly bills. Treat that deposit with the same importance as you’d treat any other bill.

Order your free credit reports

…and make sure no mistakes are bringing down your credit score.

The Fair Credit Reporting Act entitles you to free reports from the three credit bureaus every 12 months. Order them through AnnualCreditReport.com, comb through them carefully, and file disputes on the appropriate credit bureau websites for any problems you find. You may be doing great financially, but a mistake or two on your credit reports can still destroy your credit score.

Talk to a credit counselor

…at a non-profit credit counseling agency if you’re having trouble making a workable budget on your own. Many people think that credit counselors are just for people teetering on the brink of bankruptcy, but that’s not true. Legitimate counseling agencies offer a full spectrum of services, not just debt repayment plans. Find an agency that offers free counseling and educational resources and check its standing with the Better Business Bureau.

_______________________________

Thanks Liz for this post.

Tips are really useful, but also remember, mastering your money is as much a mind-game as it is about taking action on these tips.

Do you have the right mindset for success and wealth in 2012?

Watch the video to find out why mindset is so important.

{ 0 comments }

Managing your money can be tougher if you don’t understand some of the jargon.

Managing your money can be tougher if you don’t understand some of the jargon. When I blog, nothing else matters if I don’t hit ‘Publish’.

When I blog, nothing else matters if I don’t hit ‘Publish’. Yep, the peak of the stock market before the crazy ‘crashes’ of 2008 and 2009.

Yep, the peak of the stock market before the crazy ‘crashes’ of 2008 and 2009. 2011 was a crazy year to be an investor.

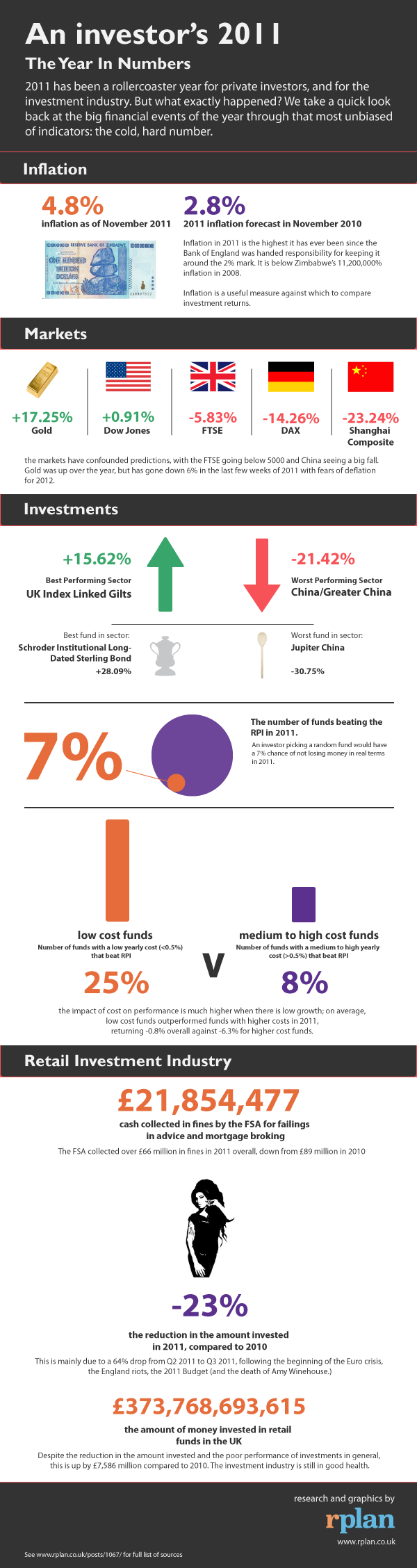

2011 was a crazy year to be an investor.

A Junior Individual Savings Account (ISA for short) is a new financial product available in the UK (I can tell you’re excited already!)

A Junior Individual Savings Account (ISA for short) is a new financial product available in the UK (I can tell you’re excited already!) I wouldn’t exactly say they are jargon free but hopefully by the end of this article you’ll have a better idea about them and know why they are so worthwhile.

I wouldn’t exactly say they are jargon free but hopefully by the end of this article you’ll have a better idea about them and know why they are so worthwhile.

.jpg) Source: www.ConstructaQuote.com

Source: www.ConstructaQuote.com