If you’re a resident of the UK, an ISA should be one of the first places you should be putting your savings.

For many, a simple cash ISA comes to mind but the interest rates are very low and your savings, whilst safe, are not likely to grow very much. Even some of the best ISAs do not pay enough to keep up with inflation, so in real terms, what the money can buy, savers can lose money.

The solution to growing your savings faster is to invest in a different kind of an ISA, such as a Stocks and Shares ISA or, one of the newest kinds of ISAs, an Innovative Finance ISA.

The solution to growing your savings faster is to invest in a different kind of an ISA, such as a Stocks and Shares ISA or, one of the newest kinds of ISAs, an Innovative Finance ISA.

Both Stocks and Shares ISAs and Innovative Finance ISAs allow savers to invest in things that have the potential to grow their money faster than cash though it does mean taking on additional risk. There is a risk because the investment value is not guaranteed to go up all the time, in fact it might go down in value for a time. If you are very unlucky, you may even lose it all depending on the how the underlying investment performs. However, there is also the potential for your investments to grow very strongly, certainly more than what is available with cash savings.

In order to manage risk it is best practice to diversify, meaning to invest in a number of different things, so if one investment goes bad, you haven’t lost everything. Diversification is an important concept to understand, meaning to spread the risk so you are not putting all your eggs in one basket.

Innovative Finance ISAs

Innovative Finance ISAs

To introduce even more options for investors and savers the UK Government introduced the Innovative Finance ISA (IFISA) in April 2016. This newer ISA allowed savers to invest in new forms of investments that promise strong returns without having to rely on more traditional stocks and shares, and offers an opportunity to investors to do some ‘good’ with the money.

One example of this new breed of investment is called Peer-to-Peer (P2P) lending.

It works like this: Those looking to borrow money used to be limited to the banks but technology now makes it easier for savers looking for a return to become mini-banks themselves. Through a peer to peer platform, investors can lend out their money to others and receive the interest paid on the loan. Those looking to borrow money now have more options than just relying on a bank,, and savers can get a better return than cash. Win Win. Best of all, the interest is received tax-free if the money is invested through an Innovative Finance ISA.

Of course there is still risk, the person making the loan might miss their payments, but for some savers, the return is worth the risk and they make lots of little loans to diversify.

Doing More With Your ISA

Doing More With Your ISA

Another form of investing offered by an Innovative Finance ISA, takes the peer-to-peer lending concept even further. Rather than helping individuals through loans, the money invested in the ISA goes into a pool to help fund legal cases for those who cannot afford to go to court to get justice. When the case is won, the legal fees are paid by the losing party and the investor gets their money back, plus interest. In the event that the court case is lost, there is insurance in place that offers some return. For investors this is a way for their money to do some good and earn a return too.

For more information about this offering within an Innovative Finance ISA click here.

With all investing, there is risk, but the potential reward could be worthwhile if you are looking to diversify your savings and investments.

It’s also important to note that, unlike cash ISAs, money invested in investments is not always covered by the Financial Services Compensation Scheme.

{ 0 comments }

While right now you’re happy working in your mundane job to merely pass the time and earn some money while you’re at it, there will eventually become a point in your life when doing that isn’t enough anymore.

While right now you’re happy working in your mundane job to merely pass the time and earn some money while you’re at it, there will eventually become a point in your life when doing that isn’t enough anymore.  you never have to work a day in your life, and this is so true.

you never have to work a day in your life, and this is so true. How Long Will it Take to Improve My Credit Score?

How Long Will it Take to Improve My Credit Score?  Factors that Improve Your Credit Score

Factors that Improve Your Credit Score  So you have decided to get a new car, but don’t want to end up in debt if things don’t work out as you expect. There are so many things you will have to consider before you sign the dotted line and drive your new wheels away. If you don’t want your car to cause you more trouble than joy, you might want to consider the below tips.

So you have decided to get a new car, but don’t want to end up in debt if things don’t work out as you expect. There are so many things you will have to consider before you sign the dotted line and drive your new wheels away. If you don’t want your car to cause you more trouble than joy, you might want to consider the below tips.  My first ever car

My first ever car

When it comes to choosing where to put your money to gain a return on your investment, there are few options as attractive as purchasing a holiday home. After all, not only do you get to see your money grow, but you and your loved ones get the benefit of using such a home as well. However, before you sink all your saving into this type of deal, it is wise to ask whether it is the best type of investment for you? Something that the post below can help you decide.

When it comes to choosing where to put your money to gain a return on your investment, there are few options as attractive as purchasing a holiday home. After all, not only do you get to see your money grow, but you and your loved ones get the benefit of using such a home as well. However, before you sink all your saving into this type of deal, it is wise to ask whether it is the best type of investment for you? Something that the post below can help you decide.  Risk #2: Your financial mindset

Risk #2: Your financial mindset Putting money into savings is a great first step if you want to grow your pennies and improve your financial situation.

Putting money into savings is a great first step if you want to grow your pennies and improve your financial situation. Get Flexible

Get Flexible

using a Junior ISA where up to £4,128 tax-free each year for their child for the 2017/18 tax year. The account becomes a basic ISA once they turn 18 meaning they access the money then, but children can get control of the money at 16. Interestingly, children aged 16 to 18 can have a Junior Isa as well as a standard ISA and they have separate allowances so lucky teens can maximise their savings if they have generous family memories or a well paid job!

using a Junior ISA where up to £4,128 tax-free each year for their child for the 2017/18 tax year. The account becomes a basic ISA once they turn 18 meaning they access the money then, but children can get control of the money at 16. Interestingly, children aged 16 to 18 can have a Junior Isa as well as a standard ISA and they have separate allowances so lucky teens can maximise their savings if they have generous family memories or a well paid job! Have you ever dreamed of building your own home?

Have you ever dreamed of building your own home? What does MMC stand for?

What does MMC stand for? Getting a Mortgage on a MMC Property

Getting a Mortgage on a MMC Property What documentation do you need?

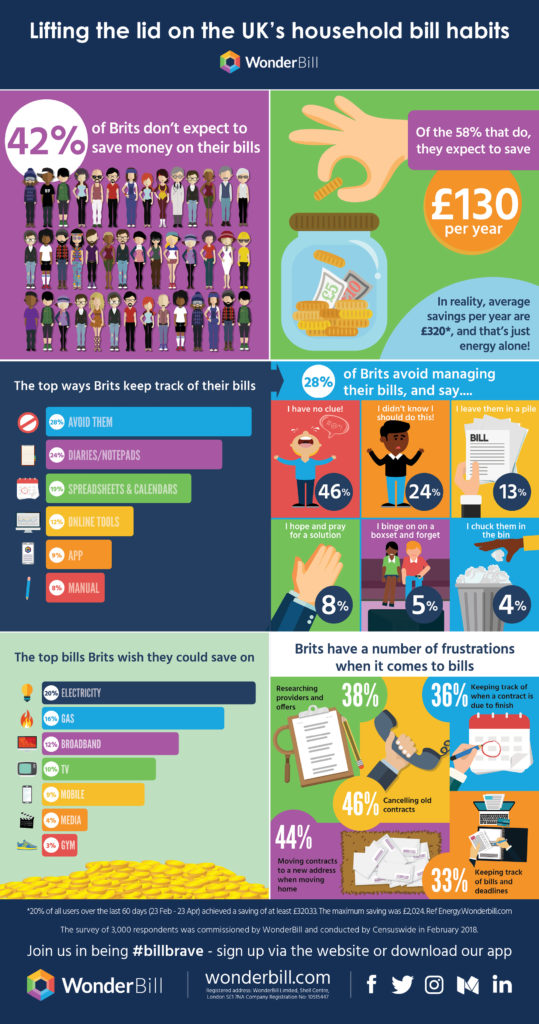

What documentation do you need? One of the most fundamental pieces of a good personal finance system is being able to pay your bills.

One of the most fundamental pieces of a good personal finance system is being able to pay your bills.  Do you have a system for managing bills? Is it working for you?

Do you have a system for managing bills? Is it working for you?

Expand Your Talents

Expand Your Talents Start a Business

Start a Business