Every birthday and Christmas of my childhood I would get a gift card from a family friend.

So would my brother and sister.

A generous gift, certainly, but the gift card could only be used in a particular stationary shop.

There’s only so many pieces of stationary a family can handle so although the gift cards were a generous present, they were not as useful and well-received as other presents.

If only we had Zeek!

Zeek is an interesting new company and website that allows you to buy and sell unwanted giftcards from a multitude of retailers, both online and offline. For sellers you can convert unwanted giftcards for cash, and for buyers you can get giftcards at a discount to their face value.

When I first went to the site, I was impressed with the variety of brands covered.

There are lots of high-street names so as a buyer you are bound to find a brand you purchase from on a regular basis.

Once you have narrowed down the brands you are interested in you can see what deals are available on the giftcards sellers have put on the site.

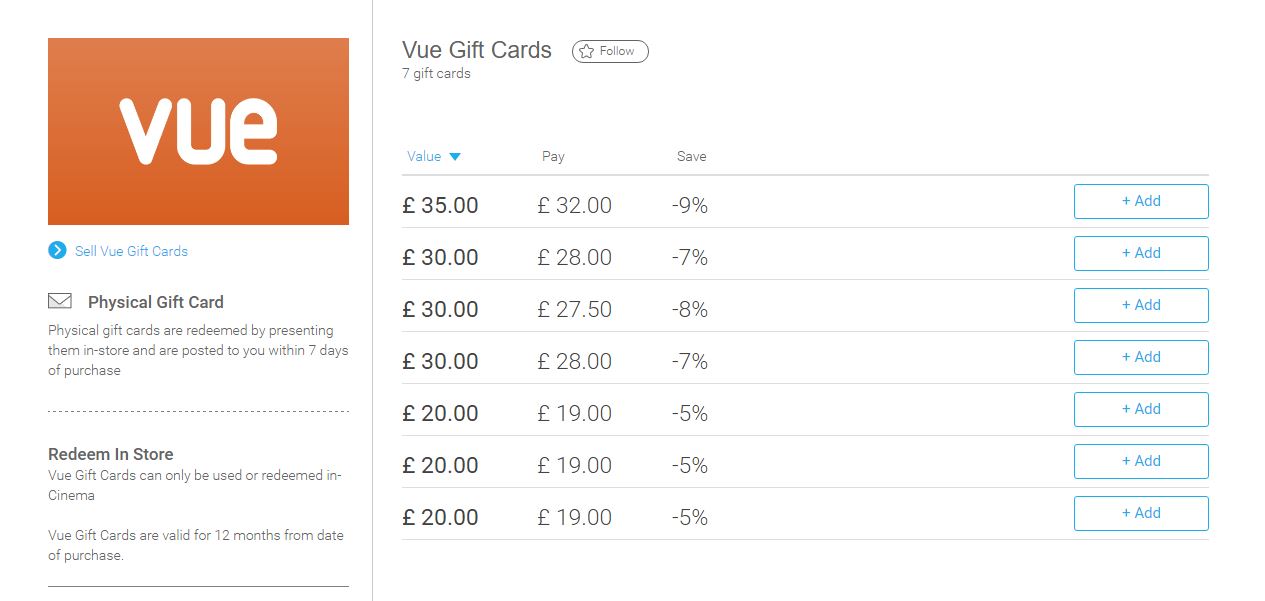

I thought I would start with a brand I was very familiar with and look at what savings I could get.

A 9% discount on cinema credit? Not bad at all!

Buying vouchers at discounted rates

The discounts are set by the sellers so they differ across giftcards and brands. The discounts are at least 1% but can be much higher. The highest I’ve seen on the site is 25% for Eurostar where a £120 voucher was selling for £90!

The discounts are higher on more niche brands and lower on bigger household names. For example, a cycle shop brand had discounts above 10% but Tesco and Amazon only had 1% discounts.

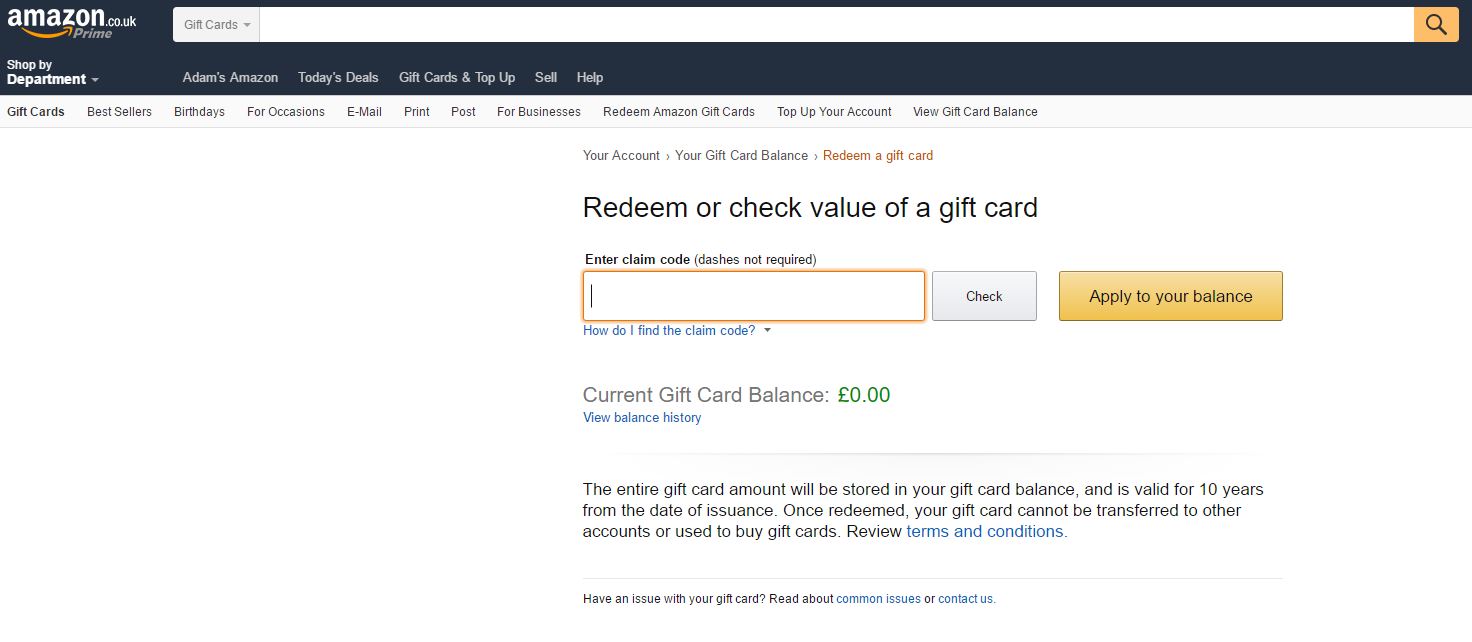

After some deliberation I went with Amazon vouchers. The discount was lower than other brands but the flexibility and immediacy made it my top choice. The deals available change from day to day and at the time I was searching only £100 vouchers were available. This was OK for me, especially with Christmas coming up but it could have been a barrier for some.

The site is dependent on sellers adding inventory to the site so you might not get exactly what you are looking for. For example as I was writing this review I went to check the site again and saw there were no Amazon.co.uk vouchers available. That said, there’s plenty of selection if you are flexible and I’m confident you could find a brand and voucher available that could save you a few pounds at least.

When looking at the gift-cards take care to note the ‘valid-to’ information. Vue gift cards are valid for 12 months from the date of original purchase for example. Amazon’s voucher was appealing because it doesn’t expire for 10 years! I also liked it was an electronic giftcard so I didn’t have to wait to receive a physical card in the post, although I have friends who have bought physical gift cards from Zeek and they told me they received the giftcards very quickly.

Payment

I liked that both card payments and Paypal could be used for payments, but was disappointed I couldn’t buy using my Paypal balance – instead the system routed me through to Paypal’s card processing page, but this is a minor niggle.

Overall the purchase was really easy to make and I got my Amazon code straight away.

Once I had the Amazon giftcode I could log into Amazon to get it credited in my account by typing in the code from Zeek.

As a buyer of giftcards I was impressed with the site and will likely use Zeek again, particularly if I was making a planned purchase. On the seller side I can imagine this site being really helpful after Christmas if I were to receive giftcards from brands I’m not that fussed about – using the site could turn an unwanted voucher into cash that can be better deployed somewhere else – paying off debt, saving it for another time, or buying something more appealing in cash.

Get £5 Zeek Free Credit

Zeek gave me some credit to review the site for Magical Penny readers, but you can get some credit too for your first purchase.

Simply use the code: 2SS35NWI for £5 free credit to use on the site. So that’s a double discount on vouchers as you are buying a voucher for below market value plus getting £5 credit straight away -definitely helpful in the run up to Christmas and beyond.

{ 0 comments }

Recent news has shown people receiving one euro for their pound

Recent news has shown people receiving one euro for their pound  Brexit hit the financial markets hard, with the pound slumping to its lowest level since the 1980s. Much of the shock in the markets came from the unexpected nature of the results, as Brexit was never ‘priced in’ to the markets. However, as always with big market movements, some people correctly predicted the trend and made huge sums of money. In this post, we focus in on one person in particular: Crispin Odey.

Brexit hit the financial markets hard, with the pound slumping to its lowest level since the 1980s. Much of the shock in the markets came from the unexpected nature of the results, as Brexit was never ‘priced in’ to the markets. However, as always with big market movements, some people correctly predicted the trend and made huge sums of money. In this post, we focus in on one person in particular: Crispin Odey. For her it’s a chance to catch up on lesson planning but for families with children, half term is often a whirlwind of activity, and costs can really add up.

For her it’s a chance to catch up on lesson planning but for families with children, half term is often a whirlwind of activity, and costs can really add up. Travel

Travel Are you a big fan of Marmite, like my girlfriend?

Are you a big fan of Marmite, like my girlfriend? Buying a new car can unleash all sorts of questions, such as:

Buying a new car can unleash all sorts of questions, such as: Whether you’re buying a car for the first time, or getting an upgrade, if the price of the car that you have set your eyes on is what you can afford, you may be eligible to purchase it on a finance scheme, provided of course that:

Whether you’re buying a car for the first time, or getting an upgrade, if the price of the car that you have set your eyes on is what you can afford, you may be eligible to purchase it on a finance scheme, provided of course that: Over 9 million people this Christmas are planning to pay for Christmas on a credit card.

Over 9 million people this Christmas are planning to pay for Christmas on a credit card.  Apply for a taxpayer identification number or TIN number easily by using an online service. These third-party services, such as IRS-EIN-TAX-ID.COM understand how complex the TIN number application is, which is why they provide you with a simplified process. With this, they have easy to understand forms which help users to enter the correct information the first time cutting down instances of application rejection due to errors.

Apply for a taxpayer identification number or TIN number easily by using an online service. These third-party services, such as IRS-EIN-TAX-ID.COM understand how complex the TIN number application is, which is why they provide you with a simplified process. With this, they have easy to understand forms which help users to enter the correct information the first time cutting down instances of application rejection due to errors. For most people, paying the bills means the need to earn a living. One can typically expect to work throughout much of their adult lives. The sad truth for some of us is that our working lives get cut short. It can happen for a variety of reasons, with the common one being a debilitating injury.

For most people, paying the bills means the need to earn a living. One can typically expect to work throughout much of their adult lives. The sad truth for some of us is that our working lives get cut short. It can happen for a variety of reasons, with the common one being a debilitating injury. Seek professional medical advice

Seek professional medical advice Find out what insurance coverage you have

Find out what insurance coverage you have See if you can make a compensation claim

See if you can make a compensation claim