Few things in life cause us more stress than a serious financial setback.

Few things in life cause us more stress than a serious financial setback.

When the world revolves around money as it can often seem to do, and when everything costs quite so much, a lack of money can be seriously worrying. You may find that you respond in ways you did not expect, such as with extreme anxiety, or you could even spiral into a depressive state. Try not to panic too much about these kinds of reactions. They are normal responses to money worries, and many people experience them at some point in their lives. You need to put yourself first and make sure that you are getting the help you need to improve your emotional and mental state – whether that is by visiting your doctor or confiding in a trusted friend or family member. Once you are feeling better and more relaxed, you can then take action to sort out your money problems once and for all. Being productive and coming up with solutions will also help you to feel better about things, and will fast-track you to getting back in the black. If you are currently in the middle of some pretty messy finances, read on to see if any of the scenarios below paint a familiar picture. Sometimes life deals us a rough hand, and it can set off a spiral of financial problems – but there is always a way out of it, providing you make the right decisions.

The dodgy deal

The dodgy deal

It’s safe to say that most of us could all do with a little more money. Whether it’s to tide us over after a big purchase, or simply because we want to treat ourselves (who doesn’t?!), very few people would turn down the opportunity to make a little extra cash. Things get worrying, however, when people forget to check if the means by which they are making said money are legitimate. It’s sad that it has come to this, but unfortunately, there are a lot of people out there who seek to exploit other people’s need to supplement their income, by enticing them into unsafe schemes and deals. A top example of this would be the pyramid scheme, which has only grown in popularity since the world went digital. It is now easier than ever for these scammers to prey on vulnerable individuals and persuade them to put money into a scheme, with the eventual promise of a huge return. However, it is very, very rare that any of these schemes actually pull through and deliver the goods. Usually, the person or company running the project will try and get as much cash out of you as possible, and then they will simply disappear without a trace, leaving you penniless and confused. Another example of losing your money to a dodgy deal could be investing in a business idea with someone you don’t entirely trust, or someone you don’t even know that well. It can be very easy to kick yourself after the whole thing has come crashing down, but beating yourself up about it won’t get you anywhere. The best thing to do is to be very mindful of the finances you do have left and to take responsible action. Gather all the evidence you have about your involvement in the scheme and take it to a court of law, or claim your losses for previous tax years. Being a victim of a Ponzi scheme can be devastating, but it doesn’t need to define your whole life.

Becoming ill/having an accident

Becoming ill/having an accident

Even the biggest control freaks among us can’t always stay in complete control of our health. Sometimes, illnesses can creep up on us when we least expect it, or we might suffer an accident that it was impossible to foresee. This can be upsetting and stressful at the best of time, but if you have to take time off work or even give up your job completely, it can be particularly devastating. However, just like with losing money to a Ponzi scheme, wallowing won’t do you much good or bring that much-needed cash into your bank account. The first thing to do is to accept your situation, as this is what will allow you to move forward in the best possible way. Then, you will be able to take a look at what your options are. If you have been in an accident that wasn’t your fault, make a point of contacting your insurance company, as you might be eligible for compensation. Or, perhaps you have battled a chronic illness all your life which has recently rendered you disabled. This, in particular, can be quite hard to accept, but try not to despair – there are options out there for you.

One would be to seek legal advice from a company such as Brown and Crouppen, who specialize helping disabled people claim the benefits and financial support that they need. Many programs also help those of us who can still work despite our illness, but who are part-time or on a low-income. This kind of support can be invaluable when you have medical bills to pay for, so take the time to see what you could be owed.

Overspending

We all probably know a handful of people who repeatedly insist that they are ‘bad with money.’ This probably means that they tend to impulse buy, or that they have a slightly dubious looking credit score. There is, however, a huge difference between being bad with money in this respect, and getting yourself into severe financial difficulties. For some of us, overspending can be a real problem, to the point that it can become an addiction of sorts. When we spend money and buy something we really like (such as an item of clothing), we get a dopamine rush, similar to the feeling an addict gets from using a drug of their choice. It might sound extreme, but it’s true: shopping can easily become an addiction, especially if you feel as though you have an image to uphold. The majority of people with bad spending habits tend to bury their heads in the sand and ignore the gravity of where their finances are heading. For example, they may ignore bills and warning letters, apply for multiple credit cards and use overdrafts recklessly. Or, on the other hand, they may turn to questionable methods of money making to fund their habit, such as gambling. All of this amounts to some pretty destructive behavior and can lead to major turmoil unless you do something about it. In order to take back control of your spending, first, confide in a trusted friend. You may not even realize the severity of your problem, so by speaking to someone else you may be able to gain perspective on the issue at hand. Then you will need to come face to face with the harsh reality of your spending habits. Sure, looking at all the debts and bills might be painful, but you need to have it all laid out in front of you so you can organize yourself properly. Visit a financial, advisor who can help you put a repayment plan in place so you can gradually clear your debts off one by one. The feeling of being back in the clear can transform your life, so by facing up to your spending, you can change things for the better.

Divorcing

Divorcing

Getting a divorce or separating from your partner can be a hugely stressful time, emotionally. The fact that it can also impact on your personal finances definitely doesn’t help things, and it’s a lot to take on at once. But as painful as it might be, spending some time sorting out your money in those early stages can save you a lot of heartache in the long run. Work out what is in your name and what is in your partner’s name, then try to come to some agreement on how you are going to split things. If your split is not unanimous and you fear that there will be a lot of conflict within these discussions, hire a lawyer or some other kind of independent mediator who will be able to act as a middleman for the two of you. Bear in mind that certain things will make this process more complicated, such as if the two of you own a business together, or if one of you has considerably more assets than the other. But providing that you approach the issue in a mature fashion, and that you don’t make any impulse investments or decisions relating to your finances, there is no reason why you can’t have the money distributed fairly and easily.

These are just a few examples of the curveballs life can throw at us regarding our personal and financial lives – so by being aware of the risks and what to do, you can make sure you run your finances, not the other way around!

{ 0 comments }

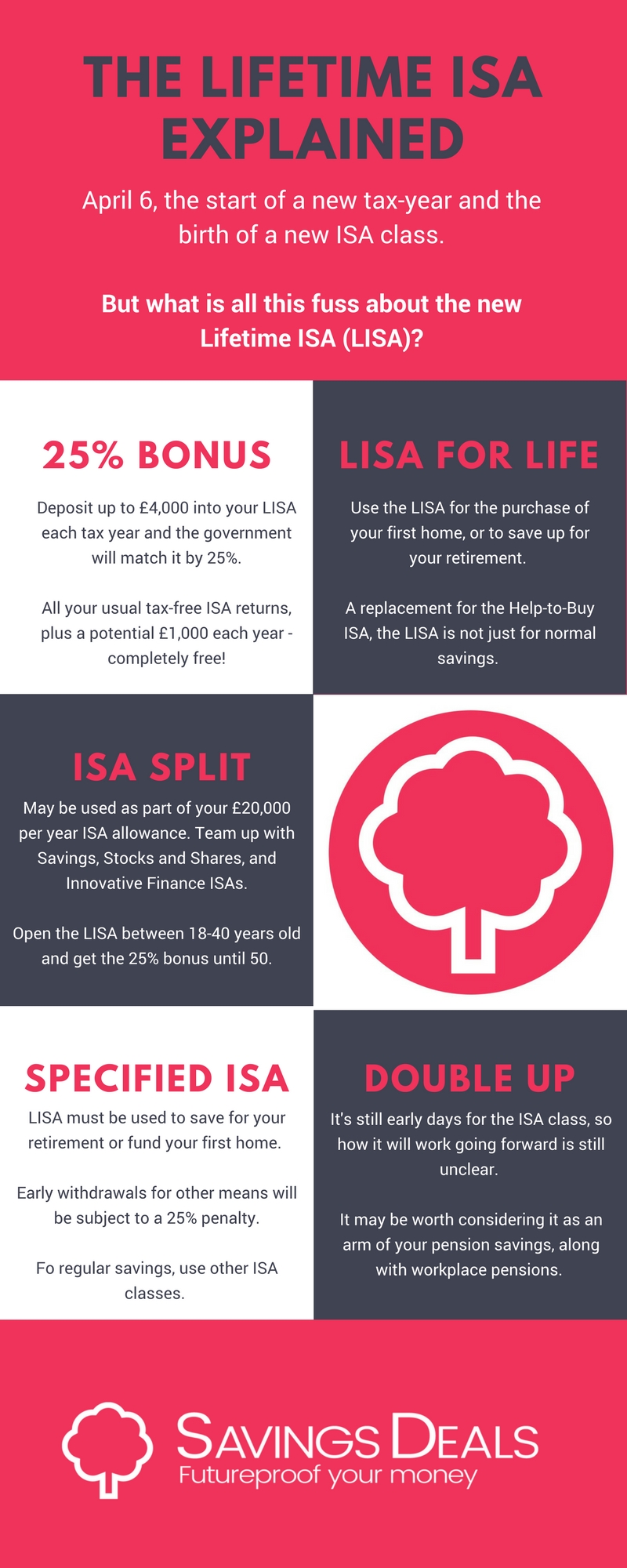

On April 6th, the start of the new financial year, a new ISA class was born.

On April 6th, the start of the new financial year, a new ISA class was born.

One of the biggest purchases you could possibly make in your adult life, is that of a house. It may be a bucket list item, but it’s one that comes with many dollar signs, some of which you simply cannot foresee. Most people think it’s a case of saving a deposit and the bank will give you a mortgage for your dream home – sadly, that’s not the case.

One of the biggest purchases you could possibly make in your adult life, is that of a house. It may be a bucket list item, but it’s one that comes with many dollar signs, some of which you simply cannot foresee. Most people think it’s a case of saving a deposit and the bank will give you a mortgage for your dream home – sadly, that’s not the case. Comparison:

Comparison: The life of a landlord is often a very busy one. A lot of people in this position find themselves having to dedicate far more time than they expected into this role. Of course, the time will often be worth the money that you get from it. But, if you were spending less time on it; the money could be even more valuable. For some, saving time in this area will be the only option. So, to help you out, this post will be going through some of the ways that you can make sure that your investment dreams are coming true. It just takes a little bit of work; but, once it’s done, you could be saving loads of time.

The life of a landlord is often a very busy one. A lot of people in this position find themselves having to dedicate far more time than they expected into this role. Of course, the time will often be worth the money that you get from it. But, if you were spending less time on it; the money could be even more valuable. For some, saving time in this area will be the only option. So, to help you out, this post will be going through some of the ways that you can make sure that your investment dreams are coming true. It just takes a little bit of work; but, once it’s done, you could be saving loads of time. Buy Properties Nearby

Buy Properties Nearby It is estimated that every day, each person makes roughly

It is estimated that every day, each person makes roughly  First, you should carefully calculate just what sort of mortgage you will be able to get. Many banks will not offer you any deal if you do not have a sufficient deposit. The standard was once 25%, but many banks expect around

First, you should carefully calculate just what sort of mortgage you will be able to get. Many banks will not offer you any deal if you do not have a sufficient deposit. The standard was once 25%, but many banks expect around  Debt Consolidation Options

Debt Consolidation Options Below, you will find all you need to know about the risks that are always worth taking, as well as details of those that you should stay away from. There is no way of being 100% certain about which risks you should and shouldn’t take. But on balance, it’s possible to predict which risks will pay off and which won’t.

Below, you will find all you need to know about the risks that are always worth taking, as well as details of those that you should stay away from. There is no way of being 100% certain about which risks you should and shouldn’t take. But on balance, it’s possible to predict which risks will pay off and which won’t. Listening to Tips and Propositions That Are Too Good to be True

Listening to Tips and Propositions That Are Too Good to be True Having No Emergency Fund

Having No Emergency Fund There are so many great ways to kick your finances into shape when you’ve let them collapse. Regaining control is not easy, but you don’t need to follow the same dull tips and rules that lots of people talk about and point you towards. Sometimes, thinking outside the box and taking a few simple steps can be enough to improve your financial situation. Here are some ideas that you should try out.

There are so many great ways to kick your finances into shape when you’ve let them collapse. Regaining control is not easy, but you don’t need to follow the same dull tips and rules that lots of people talk about and point you towards. Sometimes, thinking outside the box and taking a few simple steps can be enough to improve your financial situation. Here are some ideas that you should try out. Bad Credit Isn’t The End of the World

Bad Credit Isn’t The End of the World