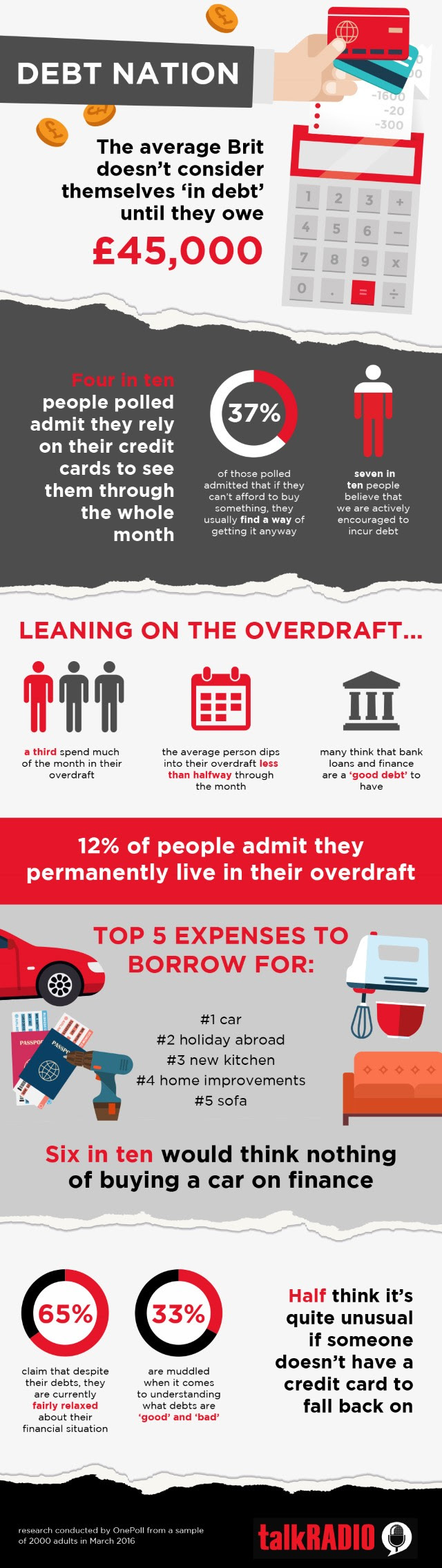

The average Brit doesn’t consider themselves ‘in debt’ until they owe £45,000, according to concerning new research.

This recent study into the financial behaviour of 2,000 adults, from this month (March 2016) by new speech radio station talkRADIO, shows the majority have a worrying lackadaisical approach to borrowing and owing money.

Four in 10 people polled admit they rely on their credit cards to see them through the whole month, and usually have a balance of at least £3,000 debt to pay, while a further third spend much of the month in their overdraft.

But it is only when the mountain of debt reaches above £45,000 that people start to panic, and realise that they need to take action to remedy their financial situation.

The research highlights that the days are long gone when an overdraft was for emergency borrowing only and a credit card was something we pulled out when there was no other option. Certainly increasing numbers are blogging about their journey out of debt, which can creep up through even perceived ‘normal’ spending.

Another research finding was the average person dips into their overdraft less than halfway through the month, with twelve per cent of respondents admitting they permanently live in their overdraft.

Source

Good and Bad Debt

When it comes to understanding what debts are ‘good’ and ‘bad’, a third of adults admit they are muddled. Council tax debt, tax debt and utilities companies chasing for payment are considered the very worst kind of debt to be in. But mortgages, student loans, finance options and bank loans are largely considered ‘good debts’ by many.

But debt, regardless of what type it is, can stop you from achieving your financial goals. Even ‘good’ debt, should be eliminated.

For more articles on Debt, read the Magical Penny Debt archive.

{ 0 comments }

According to statistics, consumer spending increased to a record high during the fourth financial quarter of 2015, and this is usually a sign of strong economic growth.

According to statistics, consumer spending increased to a record high during the fourth financial quarter of 2015, and this is usually a sign of strong economic growth.  How is Residential Stamp Duty Changing?

How is Residential Stamp Duty Changing? Deposit Dilemmas

Deposit Dilemmas  Realistic Research

Realistic Research I have needed to do a tax return for the last few years due to income derived from this very site and a few other online ventures. I also do quite a lot of paid singing work in addition to my day job as a paraplanner in a financial planning business. Completing my tax return each year has been relatively simple but keeping track of expenses for the purpose of documenting them on a tax return takes some time.

I have needed to do a tax return for the last few years due to income derived from this very site and a few other online ventures. I also do quite a lot of paid singing work in addition to my day job as a paraplanner in a financial planning business. Completing my tax return each year has been relatively simple but keeping track of expenses for the purpose of documenting them on a tax return takes some time.

Invoice discounting has a reputation of being for businesses that are facing cash flow problems. As well as being a perfect solution to slow-paying customers and shortage of capital, it is also a legitimate way to finance the growth of your business. Here we’ve explored the ways that invoice discounting could help your business if used in the right way.

Invoice discounting has a reputation of being for businesses that are facing cash flow problems. As well as being a perfect solution to slow-paying customers and shortage of capital, it is also a legitimate way to finance the growth of your business. Here we’ve explored the ways that invoice discounting could help your business if used in the right way.

The writing is on the wall for the concept of physical cash. Sure, it may have served us well for the past several centuries but in a digital age, cash is becoming obsolete at such a rapid pace that the only way our children’s children will ever get to see coins and notes will be in a museum.

The writing is on the wall for the concept of physical cash. Sure, it may have served us well for the past several centuries but in a digital age, cash is becoming obsolete at such a rapid pace that the only way our children’s children will ever get to see coins and notes will be in a museum. If Lloyds and their ilk were far from on the ball, it could well do, certainly, but something tells us that isn’t going to be the case. That something? This, from Lloyd’s Bank Head of Personal Current Accounts, Claire Garrod: “People are increasingly expecting to use new technologies to make payments rather than rely on cash. The benefits of these new developments are gradually being understood and embraced by banks and their customers, to make payments more convenient without compromising security.” (

If Lloyds and their ilk were far from on the ball, it could well do, certainly, but something tells us that isn’t going to be the case. That something? This, from Lloyd’s Bank Head of Personal Current Accounts, Claire Garrod: “People are increasingly expecting to use new technologies to make payments rather than rely on cash. The benefits of these new developments are gradually being understood and embraced by banks and their customers, to make payments more convenient without compromising security.” ( Not necessarily.

Not necessarily.