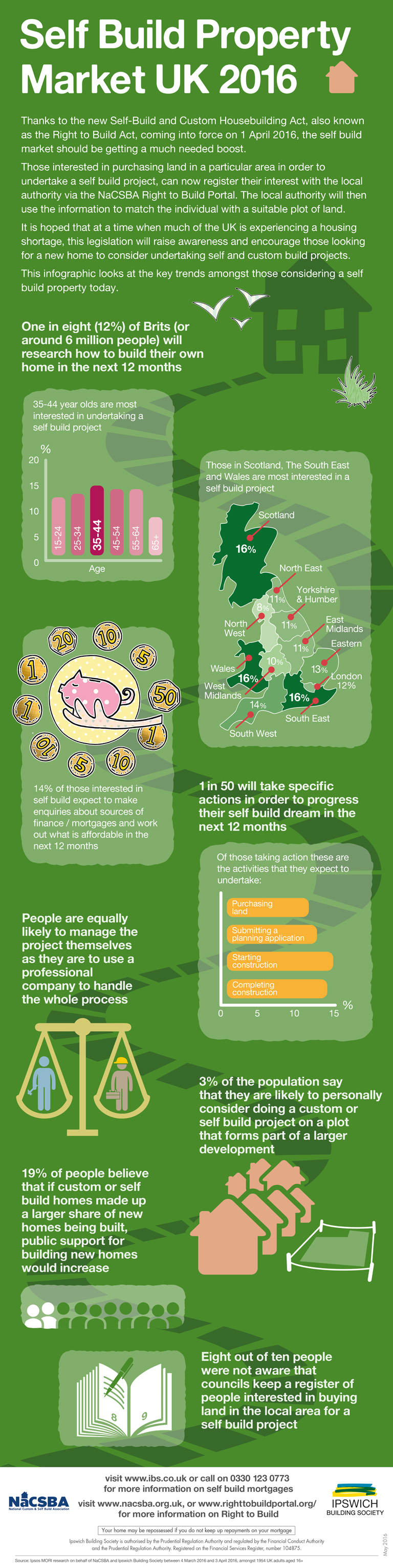

The summer is an ideal season in which to overhaul your central heating system, as your central heating will be largely off.

Before the days start shortening again, you should schedule in some time to get your boiler professionally serviced, or you could even opt to even drain the entire system and give it a thorough clean. In addition, if you are thinking of changing upgrading your radiators, this is the perfect time to do so.

Before the days start shortening again, you should schedule in some time to get your boiler professionally serviced, or you could even opt to even drain the entire system and give it a thorough clean. In addition, if you are thinking of changing upgrading your radiators, this is the perfect time to do so.

It’s understandable that many people overlook the health of their heating system in the summer, as their focus is understandably elsewhere, but this really is a great time to perform some simple checks that should ensure your system is functioning at its optimum level once the weather turns colder.

Conventional Boilers

Standard boilers are not equipped with a ‘summer mode’. Although some may have an immersion heater connected to the cylinder so that you are able to heat water independently of the boiler, this is a rather expensive way in which to get the hot water that you need.

Because the hot water and heating are not independent of each other, the boiler will still click on whenever hot water is required. The hot water is controlled by the thermostat and valves, so at some point over the summer it’s recommended that you check that these are still working properly.

Venture up into the loft, and you’ll locate the expansion and cold water storage tanks (unless you have a mains pressure-fed system in which case the cylinder will probably be located in your airing cupboard). The most important things to check over here are the overflow and the ball valve action. If your tanks are not insulated, do this as a priority. It will significantly reduce the amount of time required to reheat the water in the cylinder.

Central Heating Pump

As part of a thorough overhaul, you should also check your heating pump too, although do bear in mind that you will need to switch the heating on for a time before you do so. Check each radiator to make sure that it is heating up properly, and listen carefully to see if you can detect any rattling or grinding noises from the pump. You may find that bleeding central heating pump and other system components will be required to solve the problem.

Combi boilers

If you have a combination boiler, you may be able to switch it over the summer mode once it’s hot enough that the central heating is not required. Because a boiler of this type does not store water, they are far more energy efficient as only the water that is actually required is heated.

It is recommended that you clean your heating system once every year. You can either do this yourself by flushing it through with an industry standard cleanser, or get a professional to do it. Make sure that you add in an inhibitor when you are refilling it, as this helps to stop the system corroding.

As you are likely to notice that your cold water is rather warmer than you might like during the hotter months of the year, you could consider adjusting the temperature setting. This will result in a better mix of hot and cold water.

If you are thinking of revamping your radiators to improve the look or saleability of your property, the summer is an ideal time to carry out this task. Even if you are happy with your current radiators, you should consider improving the efficiency of your heating system by adding a thermostat. You should notice a decent reduction in your heating bill at the end of the winter.

Bleed your radiators

Many radiators will experience an issue with blockages or trapped air at some point, thus preventing water and heat from reaching the full height of the radiator. Regularly bleeding your radiators is the best way to ensure that they perform at their best. Carrying out this task in the warmer months makes sense as you will be able to identify and fix any issues before the colder weather kicks in, reducing the risk that you’ll be stuck without heating.

Many radiators will experience an issue with blockages or trapped air at some point, thus preventing water and heat from reaching the full height of the radiator. Regularly bleeding your radiators is the best way to ensure that they perform at their best. Carrying out this task in the warmer months makes sense as you will be able to identify and fix any issues before the colder weather kicks in, reducing the risk that you’ll be stuck without heating.

Power Flush

If bleeding the radiators does not eradicate the cold spots, you may need to get an expert to perform a ‘power flush’ – essentially they will flush out any slurry or sludge that may be stopping the system from working efficiently.

Stick to this simple check list, and you should find yourself enjoying a toasty warm, energy efficient home once the colder months arrive.

{ 0 comments }

The appeal of becoming an investor as opposed to a ‘passive

The appeal of becoming an investor as opposed to a ‘passive Financial goals

Financial goals Prepare the way

Prepare the way

Whenever various stock and financial markets around the world are in a state of flux, investors look towards gold to provide stability, security and peace of mind.

Whenever various stock and financial markets around the world are in a state of flux, investors look towards gold to provide stability, security and peace of mind.  But crowdfunding is not limited to Kickstarter-style projects or charity pages. There’s many other applications, particularly in the financial and investing arena.

But crowdfunding is not limited to Kickstarter-style projects or charity pages. There’s many other applications, particularly in the financial and investing arena. There are 3 different types of investment available on The House Crowd platform

There are 3 different types of investment available on The House Crowd platform One of the main appeals is the crowdfunding platform allows you to share in the potential growth of property in the UK. And it’s reassuring to know that all the properties featured on the site are vetted by experts with over 20 years of property investment experience. I don’t know about you, but it’s unlikely I would be able to seek out good investment property deals myself.

One of the main appeals is the crowdfunding platform allows you to share in the potential growth of property in the UK. And it’s reassuring to know that all the properties featured on the site are vetted by experts with over 20 years of property investment experience. I don’t know about you, but it’s unlikely I would be able to seek out good investment property deals myself. Risk tolerance

Risk tolerance Do you feel your household income needs supplementing with another income stream? Have you always enjoyed fashion and wondered if selling from a range of

Do you feel your household income needs supplementing with another income stream? Have you always enjoyed fashion and wondered if selling from a range of  With the price of gold sitting so high, the time has never been better for turning unwanted jewellery into well-needed cash. There are a few tips to bear in mind to getting the very best price possible. Knowing the golden rules of selling gold will help to ensure you get every cent of your items worth.

With the price of gold sitting so high, the time has never been better for turning unwanted jewellery into well-needed cash. There are a few tips to bear in mind to getting the very best price possible. Knowing the golden rules of selling gold will help to ensure you get every cent of your items worth. From the use of energy-efficient compressor head pumps to changing employee practices, there are many ways in which the average business can go about saving energy. Doing so is good for the environment and also a great way to keep overheads to a minimum.

From the use of energy-efficient compressor head pumps to changing employee practices, there are many ways in which the average business can go about saving energy. Doing so is good for the environment and also a great way to keep overheads to a minimum. Ensuring lights, computers, monitors and other items of electrical equipment are turned off when the office is not in use can save an organisation significant amounts of energy and noticeably cut bills. For computers and similar appliances, this means turning them off fully and not just putting them on standby.

Ensuring lights, computers, monitors and other items of electrical equipment are turned off when the office is not in use can save an organisation significant amounts of energy and noticeably cut bills. For computers and similar appliances, this means turning them off fully and not just putting them on standby.